All Categories

Featured

Table of Contents

You then acquire the cars and truck with cash. Borrowing against cash value. The disagreement made in the LIFE180 video is that you never ever obtain anywhere with a sinking fund. You diminish the fund when you pay money for the cars and truck and renew the sinking fund only to the previous degree. That is a massive misconception of the sinking fund! The cash in a sinking fund earns rate of interest.

That is how you stay on par with inflation. The sinking fund is always growing through interest from the conserving account or from your cars and truck repayments to your lorry sinking fund. It additionally happens to be what infinite financial comfortably fails to remember for the sinking fund and has outstanding recall when applied to their life insurance policy product.

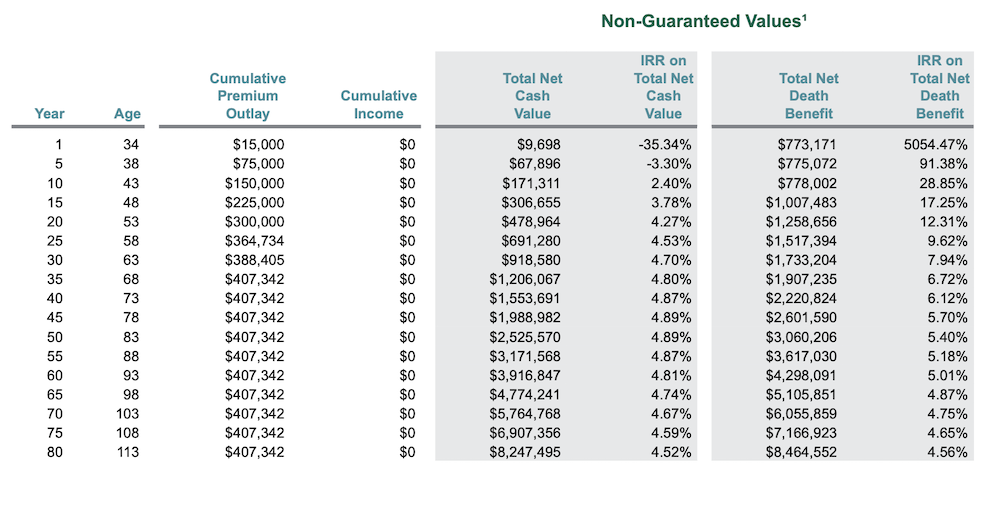

That, we are informed, is the rise in our money value in year 2. The actual boast must be that you added $220,000 to the limitless financial policy and still just have a Money Value of $207,728, a loss of $12,272 up to this point

Is Tax-free Income With Infinite Banking a better option than saving accounts?

You still have a loss regardless what column of the estimate you make use of.

Currently we transform to the longer term price of return with unlimited banking. Before we reveal truth lasting rate of return in the entire life policy projection of a marketer of boundless financial, allow's ponder the concept of linking a lot cash up in what in the video is explained as an interest-bearing account.

The only way to turn this right into a win is to make use of defective math. First, evaluate the future value calculator listed below - Whole life for Infinite Banking. (You can make use of a selection of other calculators to obtain the exact same results.) After one decade you take care of a little bit a lot more than a 2% annual rate of return.

Self-financing With Life Insurance

The concept is to get you to think you can generate income accurate borrowed from your boundless financial account while simultaneously collecting an earnings on other investments with the same money. Which leads us to the following deadly flaw. When you take a finance from your entire life insurance coverage plan what really took place? The cash money worth is a contractual promise.

The "properly structured whole life plan" bandied around by vendors of limitless financial is actually just a life insurance company that is owned by insurance policy holders and pays a returns. The only factor they pay a returns (the passion your cash money value earns while borrowed out) is due to the fact that they overcharged you for the life insurance policy.

Each insurance provider is different so my example is not a best suit to all "appropriately structured" infinite banking instances. It works like this. When you obtain a finance of "your" cash money value you pay passion. THIS IS AN ADDED FUNDING OF YOUR LIMITLESS BANKING ACCOUNT AND NOT DISCLOSED IN THE ILLUSTRATION! Picture if they would certainly have added these amounts to their sinking fund instance.

What do I need to get started with Infinite Banking For Financial Freedom?

Also if the insurance policy firm attributed your money value for 100% of the passion you are paying on the financing, you are still not getting a free ride. Infinite Banking. YOU are paying for the rate of interest attributed to your money worth for the quantities lent out! Yes, each insurance provider whole life policy "effectively structured" for infinite banking will differ

When you pass away, what happens with your entire life insurance policy? Keep in mind when I mentioned the lending from your cash worth comes from the insurance policy firms general fund? Well, that is since the cash value belongs to the insurance coverage business.

Life insurance coverage business and insurance policy agents love the principle and have sufficient factor to be blind to the deadly imperfections. In the end there are only a couple of reasons for making use of irreversible life insurance and unlimited financial is not one of them, no matter exactly how "correctly" you structure the plan.

The following approach is a variant of this approach where no financial debt is essential. Here is exactly how this technique works: You will certainly require a home loan and line of credit.

What happens if I stop using Wealth Building With Infinite Banking?

Your regular home mortgage is currently paid for a little bit more than it would have been. Rather than keeping even more than a token amount in your bank account to pay expenses you will drop the money into the LOC. You currently pay no rate of interest because that amount is no longer obtained.

If your LOC has a greater interest price than your mortgage this method runs right into troubles. If your home mortgage has a higher rate you can still utilize this strategy as long as the LOC passion price is comparable or reduced than your mortgage rate of interest rate.

The anybody can make use of (Infinite Banking wealth strategy). Infinite financial, as advertised by insurance coverage representatives, is created as a large interest-bearing account you can obtain from. Your original cash keeps earning also when obtained bent on you while the obtained funds are invested in other income generating properties, the so-called dual dip. As we saw above, the insurance coverage firm is not the warm, fuzzy entity distributing free money.

If you get rid of the insurance policy business and spend the exact same cash you will have a lot more due to the fact that you don't have intermediaries to pay. And the rate of interest price paid is probably higher, depending on current passion prices.

How do I qualify for Whole Life For Infinite Banking?

Here is the magic of infinite financial. When you borrow your very own cash you likewise pay on your own a rate of interest price.

{kind=link}

Latest Posts

Unlimited Banking Solutions

Infinity Banking

How To Take Control Of Your Finances And Be Your Own ...